Chinese GLP-1 Drugs: Mazdutide, Ecnoglutide, Ribupatide and the Global Race

Introduction#

The global obesity pharmacotherapy market, long dominated by Novo Nordisk and Eli Lilly, is facing an unprecedented challenge from Chinese pharmaceutical companies. Three Chinese-developed GLP-1 agents -- mazdutide (Innovent Biologics), ecnoglutide (Sciwind Biosciences), and ribupatide (Hengrui Pharma) -- have produced clinical data competitive with or superior to the Western incumbents, and all three are pursuing global regulatory pathways.

China's obesity market is projected to grow from $2.2 billion in 2025 to $7.5 billion by 2030. But the ambition extends well beyond domestic markets. Through strategic partnerships, licensing deals, and global Phase 3 programs, these companies are positioning their GLP-1 assets for worldwide competition. The implications for drug pricing, patient access, and the competitive landscape are significant.

The Three Contenders#

Mazdutide (Innovent Biologics): First to Chinese Approval#

Mazdutide is a dual GLP-1/glucagon receptor agonist, the same dual mechanism as survodutide and pemvidutide. It became the first dual GCG/GLP-1 agonist approved anywhere when China's NMPA granted approval for chronic weight management.

Key Clinical Data:

| Trial | Result |

|---|---|

| GLORY-1 (obesity, 48 wk) | 14.8% weight loss at 6 mg; 83% achieved 5%+ |

| GLORY-2 (obesity, 9 mg) | 20.1% weight loss at 9 mg |

| DREAMS-3 (T2D, head-to-head) | Superior to semaglutide for HbA1c and weight |

| Liver fat (GLORY-1 exploratory) | 80.2% reduction at 6 mg |

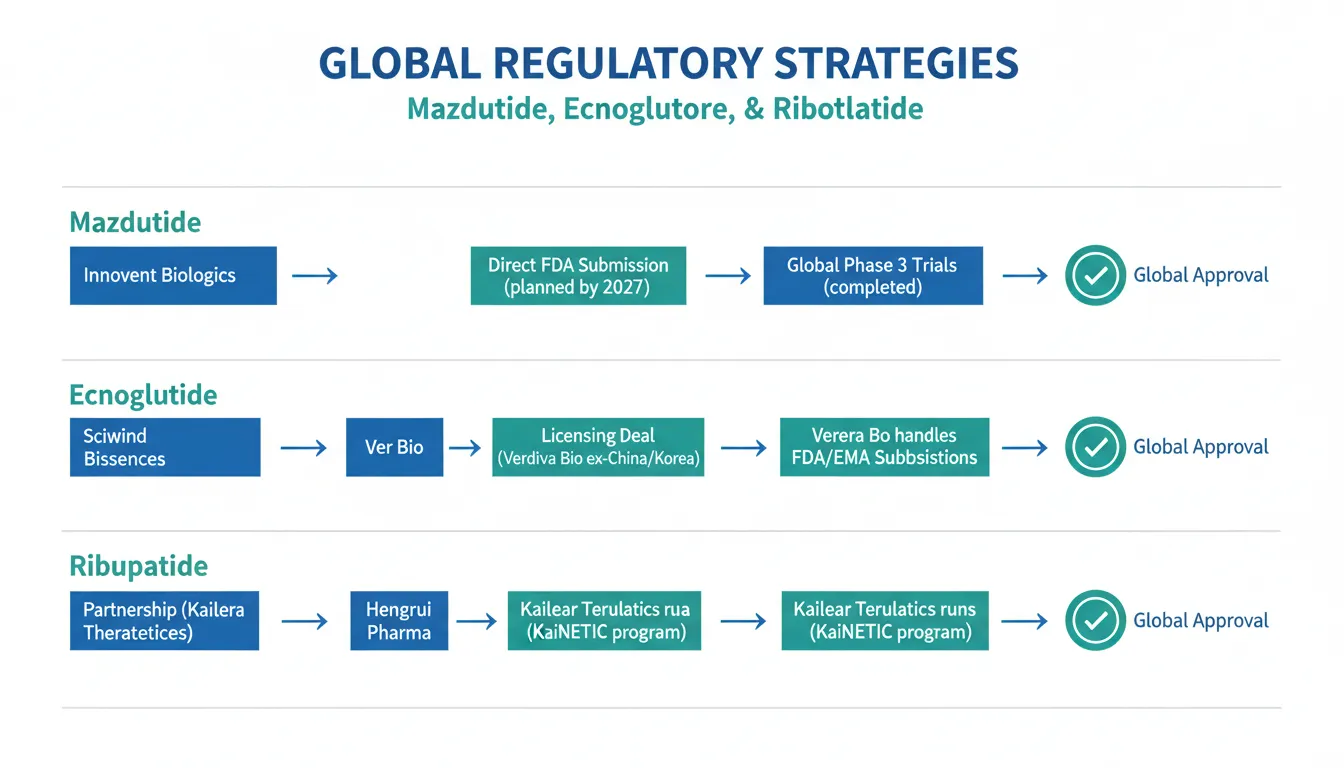

Global Strategy: Innovent is targeting FDA submission by 2027, with global Phase 3 trials planned. The 9 mg dose achieving 20.1% weight loss puts mazdutide in direct competition with tirzepatide's 20.9%. The DREAMS-3 head-to-head superiority over semaglutide for both glycemic control and weight loss is a powerful clinical differentiator.

Competitive Advantages:

- First dual GLP-1/glucagon agonist approved globally

- Head-to-head superiority over semaglutide (DREAMS-3)

- 20.1% weight loss at 9 mg approaches tirzepatide-level efficacy

- Strong liver fat reduction data (glucagon pathway)

- Established Chinese manufacturing and supply chain

Ecnoglutide (Sciwind Biosciences): Biased Signaling Innovation#

Ecnoglutide (XW003) is a cAMP signaling-biased GLP-1 receptor agonist that preferentially activates G protein pathways over beta-arrestin recruitment. This pharmacological novelty distinguishes it from all other GLP-1 agonists.

Key Clinical Data:

| Trial | Result |

|---|---|

| SLIMMER Phase 3 (obesity, 48 wk) | 15.4% weight loss at 2.4 mg; 92.8% achieved 5%+ |

| Phase 2b (Australia/NZ, 18 wk) | 11.1% weight loss at 2.4 mg, superior to liraglutide |

| Phase 2 (T2D, 20 wk) | HbA1c reduction up to 2.39% |

Global Strategy: In January 2025, Sciwind licensed oral ecnoglutide rights outside China and Korea to UK-based Verdiva Bio for approximately $70 million upfront and up to $2.4 billion in milestone payments. Sciwind is pursuing a Hong Kong IPO to fund further development. The injectable formulation's Phase 3 data (SLIMMER) positions it for Chinese regulatory filing, while the oral program advances globally through Verdiva.

Competitive Advantages:

- Novel cAMP-biased signaling (potential long-term receptor responsiveness)

- Made entirely of natural amino acids (simplified manufacturing)

- Oral formulation in development without fasting restrictions

- Phase 3 data competitive with semaglutide (15.4% vs 14.9%)

- Major global licensing deal ($2.4B milestones)

Ribupatide (Hengrui Pharma / Kailera Therapeutics): Dual GLP-1/GIP Challenger#

Ribupatide (HRS9531/KAI-9531) is a dual GLP-1/GIP receptor agonist, the same class as tirzepatide, developed by Hengrui Pharma for China and Kailera Therapeutics for global markets.

Key Clinical Data:

| Trial | Result |

|---|---|

| Phase 2 injectable (China, 36 wk) | 23.6% weight loss at 8 mg; 59% achieved 20%+ |

| Phase 3 injectable (China) | Up to 17.7% weight loss; 88% achieved 5%+ |

| Phase 2 oral (China, 26 wk) | 12.1% weight loss at 25/50 mg |

| GI tolerability (oral) | No permanent GI discontinuations |

Global Strategy: The KaiNETIC global Phase 3 program (KaiNETIC-1, -2, -3) evaluates weekly injectable ribupatide doses up to 10 mg over 76 weeks across multiple countries. Kailera plans to initiate a global Phase 2 for oral ribupatide in 2026. This dual injectable + oral strategy mirrors the development approach that Eli Lilly is taking with tirzepatide and orforglipron.

Competitive Advantages:

- Same dual GLP-1/GIP mechanism as tirzepatide (the market leader)

- Injectable Phase 2 weight loss of 23.6% at 36 weeks (no plateau)

- Oral formulation with 12.1% weight loss and excellent GI tolerability

- Established global Phase 3 program (KaiNETIC) with Kailera partnership

- Both formulations in parallel development

Comparative Overview#

| Feature | Mazdutide | Ecnoglutide | Ribupatide |

|---|---|---|---|

| Developer | Innovent Biologics | Sciwind Biosciences | Hengrui / Kailera |

| Mechanism | GLP-1 + Glucagon | GLP-1 (biased) | GLP-1 + GIP |

| Max weight loss | 20.1% (9 mg) | 15.4% (2.4 mg) | 23.6% (8 mg injectable) |

| Chinese approval | Yes (obesity) | Filing expected | Not yet |

| Global Phase 3 | Planned | Via Verdiva | KaiNETIC (initiated) |

| Oral formulation | No | In development | 12.1% at 26 wk |

| Head-to-head vs sema | DREAMS-3 (superior) | None | None |

| Liver-specific data | 80.2% fat reduction | None | None |

| Global partner | Self (planned FDA) | Verdiva ($2.4B deal) | Kailera Therapeutics |

Implications for the Global Market#

Pricing Pressure#

Chinese GLP-1 drugs could dramatically alter the economics of obesity treatment. Mazdutide is priced significantly lower in China than Wegovy or Mounjaro in the US. If these agents gain global approval, competitive pricing could force Novo Nordisk and Eli Lilly to reduce prices or risk losing market share, particularly in price-sensitive markets.

Supply Chain Diversification#

Global GLP-1 supply has been constrained, with semaglutide and tirzepatide experiencing shortages. Chinese manufacturers with established peptide production capacity could help alleviate supply constraints, particularly if multiple agents gain approval.

Regulatory Pathways#

Chinese pharma companies are pursuing different regulatory strategies:

- Mazdutide: Direct FDA filing planned (Innovent has US-based regulatory experience from partnering with Lilly on other programs)

- Ecnoglutide: Licensed to Verdiva for ex-China/Korea rights, leveraging a Western partner for FDA/EMA submissions

- Ribupatide: Kailera Therapeutics (US-based) running global Phase 3 with Hengrui partnership

Innovation Differentiation#

Each Chinese agent offers something the Western incumbents do not:

- Mazdutide adds glucagon receptor activation (liver benefits) that tirzepatide lacks

- Ecnoglutide offers biased GLP-1 signaling not found in any approved agent

- Ribupatide provides an oral dual GLP-1/GIP option that tirzepatide does not have

Challenges and Risks#

Regulatory Hurdles#

FDA approval requires global Phase 3 data in diverse populations. Trials conducted primarily in Chinese populations may not directly translate to global regulatory filings without bridging studies or multinational trials.

Evidence Gaps#

Much of the Chinese GLP-1 data comes from Chinese-only populations with different baseline BMI distributions, body composition, and metabolic characteristics. Global Phase 3 trials with diverse enrollment are essential for regulatory acceptance and clinical confidence.

Competition Timeline#

By the time Chinese agents reach global markets, the competitive landscape may have shifted. Retatrutide (triple agonist), amycretin (unimolecular GLP-1/amylin), CagriSema, and oral orforglipron may already be established.

Conclusion#

Chinese pharmaceutical companies have produced GLP-1 agents with clinical data competitive with the Western incumbents. Mazdutide's NMPA approval, GLORY-2 weight loss of 20.1%, and head-to-head superiority over semaglutide position Innovent as the most advanced Chinese challenger. Ribupatide's 23.6% injectable weight loss and oral formulation give Hengrui/Kailera a direct path to competing with tirzepatide. Ecnoglutide's biased signaling and Verdiva licensing deal represent a novel pharmacological approach entering global development.

The impact on the global obesity treatment market will depend on regulatory success, pricing strategy, and whether these agents can replicate their Chinese clinical results in diverse global populations. If they succeed, the GLP-1 market will shift from a Novo Nordisk/Eli Lilly duopoly to a genuinely competitive global landscape, which would ultimately benefit patients through lower prices and broader access.

Related Peptide Profiles#

Learn more about the peptides discussed in this article:

- Mazdutide Overview and Research Guide

- Mazdutide Dosing Protocols

- Mazdutide Side Effects and Safety

- Ecnoglutide Overview and Research Guide

- Ecnoglutide Dosing Protocols

- Ecnoglutide Side Effects and Safety

- Ribupatide Overview and Research Guide

- Ribupatide Dosing Protocols

- Ribupatide Side Effects and Safety

- Semaglutide Overview and Research Guide

- Semaglutide Dosing Protocols

- Semaglutide Side Effects and Safety

- Tirzepatide Overview and Research Guide

- Tirzepatide Dosing Protocols

- Tirzepatide Side Effects and Safety

{kind=link}

Frequently Asked Questions About Chinese GLP-1 Drugs: Mazdutide, Ecnoglutide, Ribupatide and the Global Race

What does this article cover?

Research review of Chinese pharmaceutical companies entering the global GLP-1 obesity market, covering mazdutide (Innovent), ecnoglutide (Sciwind), and ribupatide (Hengrui) clinical data and global expansion strategies. This research review is for educational purposes only and does not constitute medical advice.

Which peptides are discussed in this article?

This article covers Mazdutide, Ecnoglutide, Ribupatide, Semaglutide, Tirzepatide. Key context: Mazdutide (Dual GLP-1/glucagon agonist approved in China for obesity. GLORY-2 showed 20.1% weight loss at 9 ...); Ecnoglutide (cAMP-biased GLP-1 agonist by Sciwind. Phase 3 SLIMMER showed 15.4% weight loss at 48 weeks. Licen...); Ribupatide (Dual GLP-1/GIP agonist by Hengrui/Kailera. Injectable showed 23.6% weight loss in Phase 2. Oral s...). Each peptide is discussed based on available research evidence.

What level of evidence does this research review cover?

This research review examines published preclinical and clinical studies related to the peptides discussed. Evidence quality varies between peptides and indications. The article distinguishes between FDA-approved uses and investigational applications where applicable.

What are the key takeaways from this article?

The main findings covered in this article include: Dual GLP-1/glucagon agonist approved in China for obesity. GLORY-2 showed 20.1% weight loss at 9 .... cAMP-biased GLP-1 agonist by Sciwind. Phase 3 SLIMMER showed 15.4% weight loss at 48 weeks. Licen.... Dual GLP-1/GIP agonist by Hengrui/Kailera. Injectable showed 23.6% weight loss in Phase 2. Oral s.... These takeaways are based on the research data available at the time of publication.

What is Mazdutide and why is it significant?

Mazdutide is a peptide discussed in this article because: Dual GLP-1/glucagon agonist approved in China for obesity. GLORY-2 showed 20.1% weight loss at 9 mg. DREAMS-3 showed superiority over semaglutide. Innovent targeting FDA submission by 2027.. For a complete profile of Mazdutide, see the dedicated peptide page on this site.

Continue reading this research review

Free access to the complete analysis with citations and evidence ratings.

150+ peptide profiles · 30+ comparisons · 18 research tools

Medical Disclaimer

This website is for educational and informational purposes only. The information provided is not intended to diagnose, treat, cure, or prevent any disease. Always consult with a qualified healthcare professional before using any peptide or supplement.

Join 2,000+ researchers getting biweekly updates

Enjoyed this article?

The Research Briefing delivers deep-dives like this biweekly — plus new study breakdowns, safety updates, and tool announcements.

Free forever. No spam. Unsubscribe in one click.

Where to Find These Peptides

Continue Exploring

Peptide Profiles

Keep Reading

GLP-1 Drugs for MASH and Liver Disease: Beyond Weight Loss

Research review of GLP-1 and multi-receptor agonists for MASH (metabolic dysfunction-associated steatohepatitis), including survodutide, pemvidutide, mazdutide, semaglutide, and tirzepatide liver-specific clinical data.

Peptides in Clinical Trials 2026: The Most Promising Pipeline

A research-focused overview of the most promising peptides in clinical trials as of 2026, including Retatrutide Phase 3 TRIUMPH data, Survodutide, Mazdutide, Ecnoglutide, and other emerging compounds reshaping metabolic medicine.

Weight Loss Peptides: Mechanisms, Evidence, and How They Compare

A mechanism-focused guide to weight loss peptides — how GLP-1, GIP, and glucagon pathways drive fat loss, how single, dual, and triple agonists compare, and what the clinical evidence actually shows.

You Might Also Like

Related content you may find interesting